How To Save R709 000 Interest Over 20 Years On A R1 Million Home Loan

A very informative article today by Moneyweb / Hilton Tarrant (YFM) spells out some of the best financial advice all homeowners can possibly receive - on how disciplined additional monthly home loan payments can save you literally hundreds of thousands of Rand over the 20 year home loan period.

According to Tarrant, in the same way the power of compound interest works to your advantage when saving over the long term, so it works against you in the largest purchase most people will make: their home loan. Over a 20-year period, the average home buyer will spend a significant amount of time - and a significant amount of money - paying back compounded interest.

While it is obvious that paying additional amounts into a bond monthly, no matter how little, will make a big difference over the loan term, most people don't realise just how big an impact this can have.

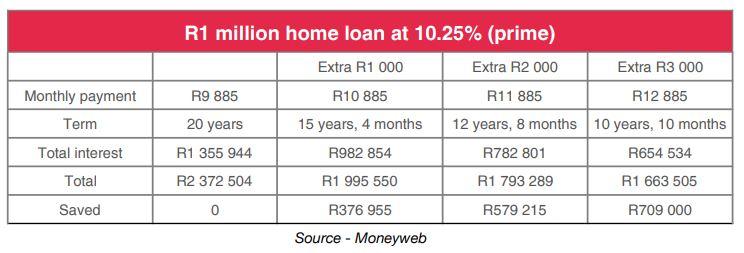

Using the example of a R1 million home loan, with a monthly repayment of around R9 900 (including service fees), even an additional R1 000 a month will take almost a quarter (!) off the span of the loan.

Paying an additional R3 000 a month on a R1 million home loan will practically halve your term and, in so doing, save a total of more than R700 000 in interest and service fees! This is a LOT of money.

You might be rolling your eyes wondering where on earth you are expected to get an additional R3 000 a month from ... that requires discipline and, crucially, not over-extending yourself when you buy a property.

A simple solution

In fact, buying a house that is 20% or 30% below what you can (or think you can) afford is possibly one of the most valuable financial decisions you could ever make.

On a R2 million home loan, making a meaningful dent in the term (and saving a ton of interest) is a bigger ask - the numbers are larger! Minimum monthly repayments will be around R19 700, and an extra R1 000 a month is not going to make that big a dent. But R4 000 extra each month translates to a R1.1 million saving in interest and fees. The term won't halve at this rate (it goes down to just under 13 years), but the total repaid is R3.6 million versus R4.7 million if you simply pay the minimum amount.

The calculations above are very simplistic, as they assume an almost robotic level of saving: a specific amount every single month. Life doesn't work that way. Some months may be higher; others lower. It also doesn't assume any adjustment for inflation, or account for changes in interest rates (which are likely).

What one should be doing - in an ideal world - is increasing your extra payments into a bond with inflation annually. In a benign interest-rate environment, this ought to be very easy. Your standard monthly repayment won't change materially, effectively becoming 'cheaper' or more affordable over time. In just five years, a repayment of R9 800 a month will be the equivalent of around R7 500 in today's money (assuming inflation of 5% a year). It should - in theory at least - become easier over time to find an additional R1 000 or R2 000 or R3 000 a month.

You will effectively be 'saving' into a home loan account, which has one advantage: you're able to access the additional capital paid at any time. For undisciplined savers, this is an obvious disadvantage as the temptation might be there to dip into these 'savings' for 'emergencies'. Treating these extra payments into a home loan as a one-way transfer (only into the account) is one way of maintaining the discipline.

Now, any additional payments into a bond shouldn't (necessarily) be at the expense of other long-term savings, such as saving for retirement. That's an entirely separate discussion, which requires input from a certified financial planner

* Hilton Tarrant works at YFM. He can still be contacted at hilton@moneyweb.co.za.