What You Need To Know About Antenuptial Contracts & Property

Category Legal Information

The matrimonial property system which you choose will affect your financial future and the position of your assets. It is therefore important that you make on informed choice. You can choose between a marriage in community of property or a marriage out of community of property. In the case of out of community of property, you will have to decide whether the accrual system should be made applicable to your marriage. If you decide to be married out of community, an Antenuptial Contract have to be registered in the Deeds Office within three (3) months of being concluded. One specific system is not necessarily the best for all couples

It all depends on the individual needs and circumstances of each couple. It is also a good time to consider preparing a Will, once you are married. It is also possible to enter into a religious marriage or a customary marriage. Please consult one of our attorneys for more information on which process should be followed in such an instance.

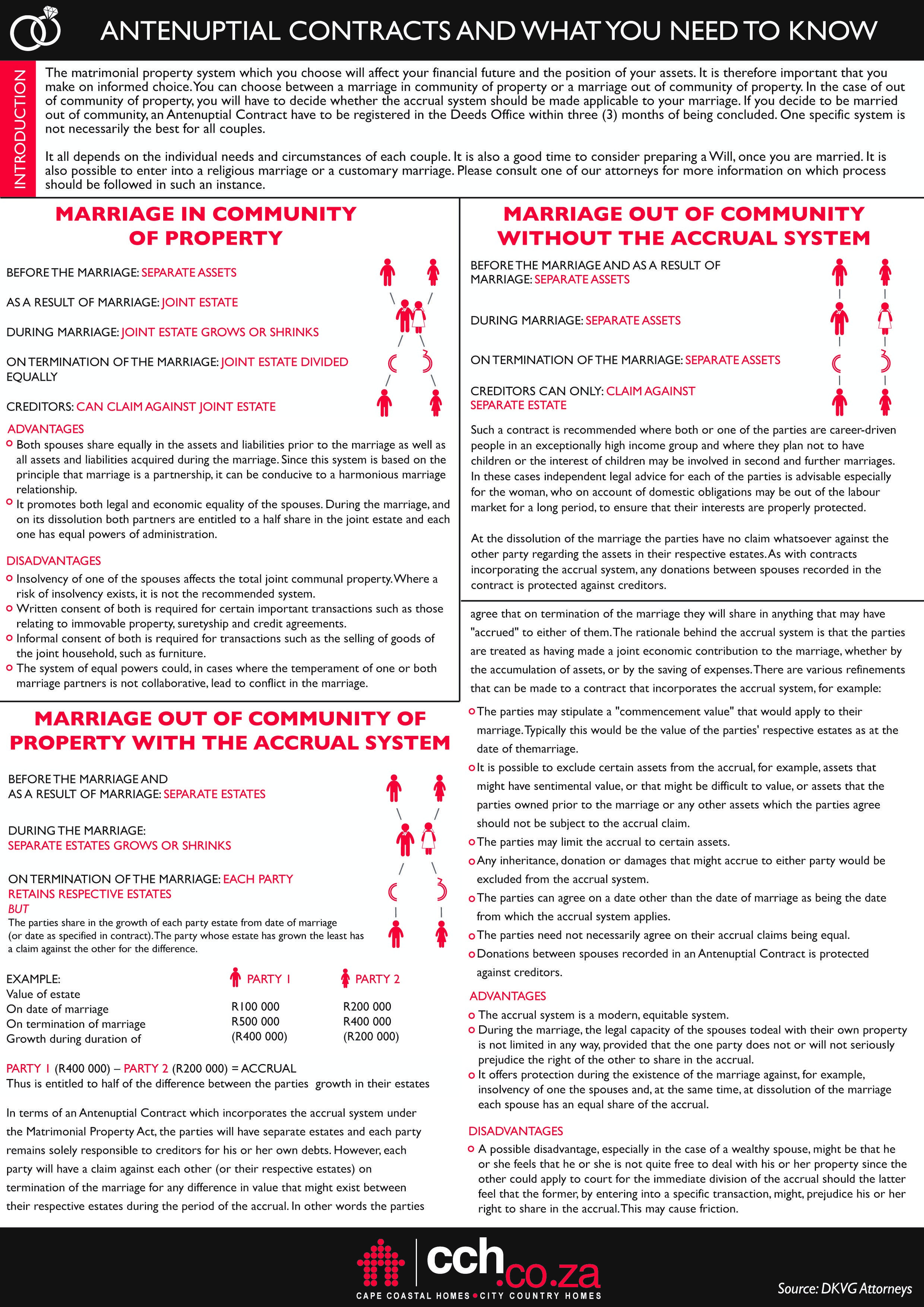

MARRIAGE IN COMMUNITY OF PROPERTY

BEFORE THE MARRIAGE: SEPARATE ASSETS

AS A RESULT OF MARRIAGE: JOINT ESTATE

DURING MARRIAGE: JOINT ESTATE GROWS OR SHRINKS

ON TERMINATION OF THE MARRIAGE: JOINT ESTATE DIVIDED EQUALLY

CREDITORS: CAN CLAIM AGAINST JOINT ESTATE

Advantages

Both spouses share equally in the assets and liabilities prior to the marriage as well as all assets and liabilities acquired during the marriage. Since this system is based on the principle that marriage is a partnership, it can be conducive to a harmonious marriage relationship.

It promotes both legal and economic equality of the spouses. During the marriage, and on its dissolution both partners are entitled to a half share in the joint estate and each one has equal powers of administration.

Disadvantages

Insolvency of one of the spouses affects the total joint communal property. Where a risk of insolvency exists, it is not the recommended system.

Written consent of both is required for certain important transactions such as those relating to immovable property, suretyship and credit agreements.

Informal consent of both is required for transactions such as the selling of goods of the joint household, such as furniture.

The system of equal powers could, in cases where the temperament of one or both marriage partners is not collaborative, lead to conflict in the marriage.

MARRIAGE OUT OF COMMUNITY WITHOUT THE ACCRUAL SYSTEM

BEFORE THE MARRIAGE AND AS A RESULT OF MARRIAGE: SEPARATE ASSETS

DURING MARRIAGE: SEPARATE ASSETS

ON TERMINATION OF THE MARRIAGE: SEPARATE ASSETS

CREDITORS CAN ONLY: CLAIM AGAINST SEPARATE ESTATE

Such a contract is recommended where both or one of the parties are career-driven people in an exceptionally high income group and where they plan not to have children or the interest of children may be involved in second and further marriages. In these cases independent legal advice for each of the parties is advisable especially for the woman, who on account of domestic obligations may be out of the labour market for a long period, to ensure that their interests are properly protected.

At the dissolution of the marriage the parties have no claim whatsoever against the other party regarding the assets in their respective estates. As with contracts incorporating the accrual system, any donations between spouses recorded in the contract is protected against creditors.

MARRIAGE OUT OF COMMUNITY OF PROPERTY WITH THE ACCRUAL SYSTEM

BEFORE THE MARRIAGE ANDAS A RESULT OF MARRIAGE: SEPARATE ESTATES

DURING THE MARRIAGE: SEPARATE ESTATES GROWS OR SHRINKS

ON TERMINATION OF THE MARRIAGE: EACH PARTY RETAINS RESPECTIVE ESTATES

BUT

The parties share in the growth of each party estate from date of marriage

(or date as specified in contract). The party whose estate has grown the least has

a claim against the other for the difference.

EXAMPLE: PARTY 1 PARTY 2

Value of estate

On date of marriage R100 000 R200 000

On termination of marriage R500 000 R400 000

Growth during duration of (R400 000) (R200 000)

PARTY 1 (R400 000) – PARTY 2 (R200 000) = ACCRUAL

Thus is entitled to half of the difference between the parties growth in their estates.

In terms of an Antenuptial Contract which incorporates the accrual system under the Matrimonial Property Act, the parties will have separate estates and each party remains solely responsible to creditors for his or her own debts. However, each

party will have a claim against each other (or their respective estates) on termination of the marriage for any difference in value that might exist between their respective estates during the period of the accrual. In other words the parties agree that on termination of the marriage they will share in anything that may have "accrued" to either of them. The rationale behind the accrual system is that the parties are treated as having made a joint economic contribution to the marriage, whether by the accumulation of assets, or by the saving of expenses.

There are various refinements that can be made to a contract that incorporates the accrual system, for example:

The parties may stipulate a "commencement value" that would apply to their marriage. Typically this would be the value of the parties' respective estates as at the date of themarriage.

It is possible to exclude certain assets from the accrual, for example, assets that might have sentimental value, or that might be difficult to value, or assets that the parties owned prior to the marriage or any other assets which the parties agree should not be subject to the accrual claim. The parties may limit the accrual to certain assets.

Any inheritance, donation or damages that might accrue to either party would be excluded from the accrual system.

The parties can agree on a date other than the date of marriage as being the date from which the accrual system applies.

The parties need not necessarily agree on their accrual claims being equal.

Donations between spouses recorded in an Antenuptial Contract is protected against creditors.

Advantages

The accrual system is a modern, equitable system. During the marriage, the legal capacity of the spouses todeal with their own property is not limited in any way, provided that the one party does not or will not seriouslyprejudice the right of the other to share in the accrual. It offers protection during the existence of the marriage against, for example, insolvency of one the spouses and, at the same time, at dissolution of the marriage each spouse has an equal share of the accrual.

Disadvantages

A possible disadvantage, especially in the case of a wealthy spouse, might be that he or she feels that he or she is not quite free to deal with his or her property since the other could apply to court for the immediate division of the accrual should the latter feel that the former, by entering into a specific transaction, might, prejudice his or her right to share in the accrual. This may cause friction.

Author DKVG Attorneys

Published 04 Jul 2018 / Views 9