5 Indicators To Follow In South African Property Market

It is important for all property owners and would be owners to keep an eye on the following 5 indicators as a means to measure the status of property market – i.e. in what stage the property cycle is at present:

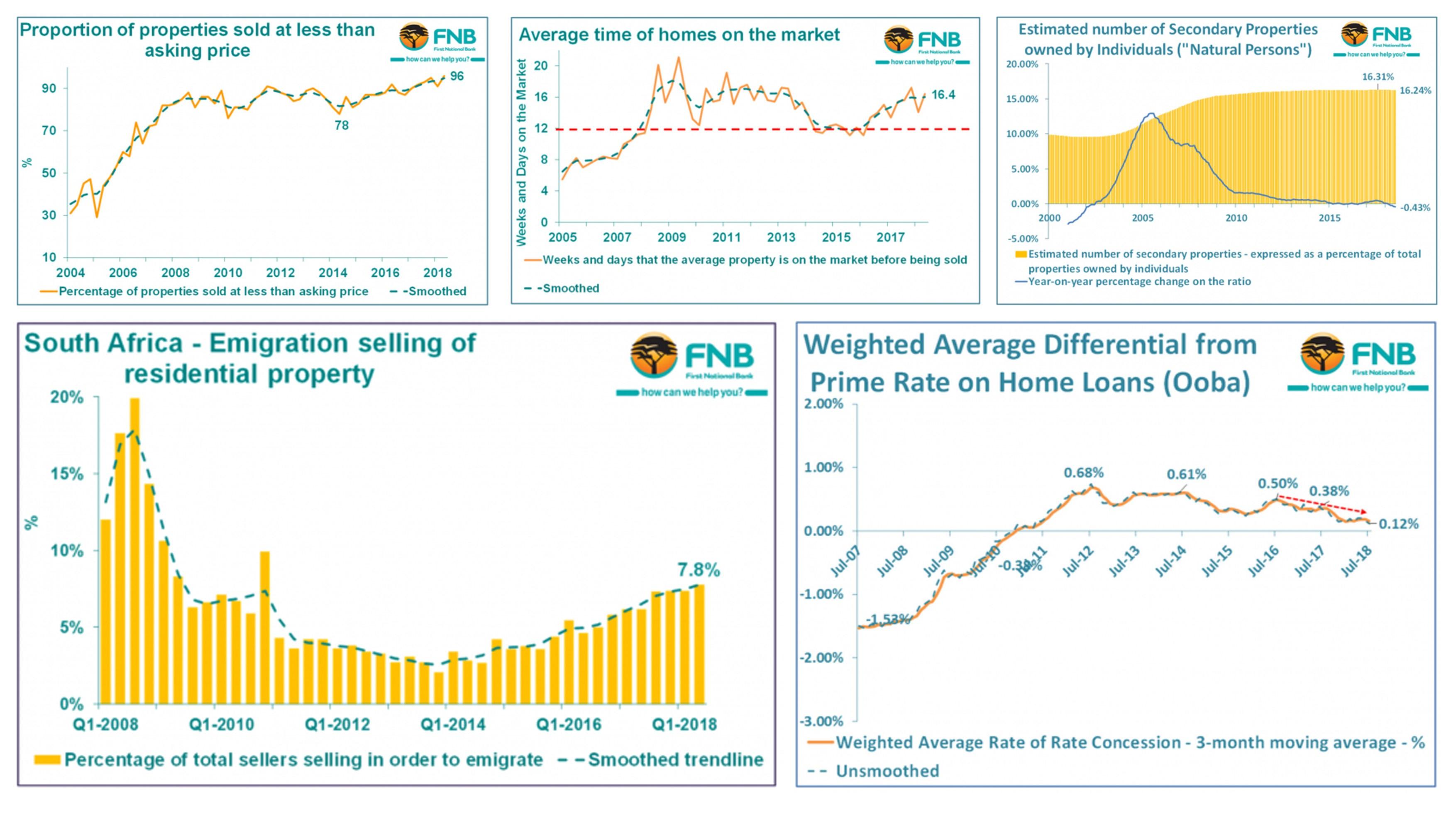

(1) proportion of properties sold for less than asking price;

(2) property average time on market;

(3) estimated number of secondary home ownership by individuals;

(4) emigration selling of residential property;

(5) how competitive is the home loan market.

According to Hylton Tarrant (Moneyweb) the residential property market has been flat in real terms over the past decade. But FNB’s August House Price Index reveals a number of details and trends that are not as apparent, especially when looking at the data month-by-month.

1. 96% of sellers have had to drop their selling price

By the second quarter of 2018 (which the August Property Barometer reports on), 96 of every 100 sellers had to drop their asking price. John Loos, household and property sector strategist at FNB, cautions about volatility between quarters (91% in Q1), but this is up significantly from 78% in 2014.

2. The average time of homes on the market is 114 days (16,4 weeks)

On average, houses are now on the market for a lot longer. The current average, from the bank’s Estate Agent Survey, is 16 weeks and four days, “noticeably” higher than the 11 weeks and one day in early 2016. The current length of time is not too far off historical highs over the past decade. The 12-week mark is “more or less” what FNB sees as equilibrium.

3. Secondary home ownership has been flat for roughly five years

“Secondary properties, as expressed as a percentage of total properties owned by individuals, has declined mildly of late,” says Loos. As of July, this number is at 16.24% from 16.31% roughly a year prior. Secondary residential buying (not ownership) has seen a noticeable decline as a percentage of total home buying. In Q2, this number had declined to 9.91% from a medium-term high of 14.47% in the first quarter of last year.

4. Emigration selling of residential property has doubled since 2013

The survey tracks three non-cyclical motives for selling: due to a change in family structure, for safety and security reasons, and in order to emigrate. Loos says the “former two have moved more or less sideways in recent years, but emigration-related selling has risen noticeably since 2013 on the back of weakening sentiment in South Africa often related to concerns over its long term policy and political direction. From a low of 2% of total selling, the emigration motive has risen to 7.8% of total selling by the second quarter of 2018.”

5. The home loan market is more competitive

On the plus side, Loos says the “mediocre” growth in the market has “seemingly encouraged a more competitive mortgage lending environment.” He cites stats from bond originator Ooba, which, when collated into an ‘effective approval rate’, shows a significant improvement of eight percentage points from 66.4% in the three months to September 2016 to 74.4% in the three months to July 2018. Home loan pricing has also been squeezed. Over a similar period, “the average weighted differential from prime rate, charged by mortgage lenders on new loans approved through Ooba, has declined from +0.5 of a percentage point above prime rate as at July 2016 to +0.12 of a percentage point above prime rate as at July 2018.”

FNB’s House Price Index slowed to 3.5%, from a revised 3.9% year-on-year in July. Using CPI data for July (August figures are not yet available), Loos says that real house prices declined by 1.2% in the month (inflation was 5.1%).